The modern franchise sector has evolved into a cornerstone of the global economy, contributing over $800 billion to the United States’ annual gross domestic product. While the franchise model offers a proven operational playbook and established brand recognition, the trajectory of a franchise—whether it plateaus as a single-unit operation or scales into a multi-regional enterprise—is increasingly dictated by an operator’s ability to navigate the complex world of commercial finance. In an era of fluctuating interest rates and tightening credit standards, understanding the nuances of how lenders evaluate brand strength, unit economics, and operator experience has become the primary differentiator for successful business owners.

The Evolution of Franchise Underwriting

Historically, securing a business loan was a localized process rooted in personal relationships and basic creditworthiness. However, the current lending environment has transitioned toward a sophisticated, data-driven methodology. Lenders no longer view franchises as monolithic entities; instead, they employ granular analysis to assess the viability of a specific concept within a specific market.

Today’s underwriting process prioritizes the "Three Pillars of Franchise Risk": the strength of the franchisor, the historical performance of the specific brand, and the operational track record of the individual franchisee. Lenders scrutinize the Franchise Disclosure Document (FDD), specifically Item 19, which provides representations of financial performance. Concepts with high "system-wide sales" but low "unit-level profitability" are increasingly flagged as high-risk, regardless of the brand’s household name status.

The Strategic Importance of the SBA 7(a) and 504 Programs

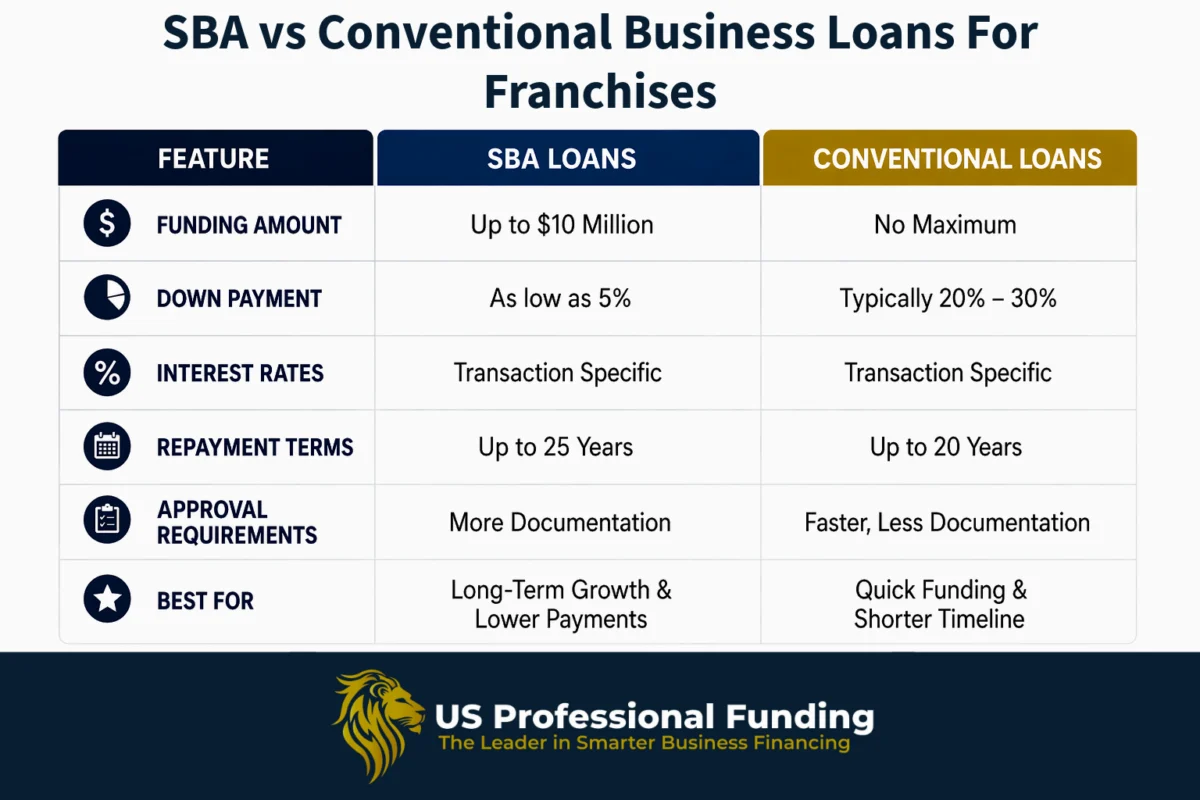

For the majority of franchise operators, the Small Business Administration (SBA) remains the most viable path toward acquisition and expansion. The SBA does not lend money directly but provides a government guarantee to the bank, reducing the lender’s risk and allowing for more flexible terms.

The SBA 7(a) loan program is the "Swiss Army Knife" of franchise finance, used for everything from working capital and equipment to leasehold improvements and debt refinancing. With loan caps typically at $5 million, it offers longer amortization periods—often 10 years for business acquisitions and 25 years for real estate—which preserves the operator’s monthly cash flow.

In contrast, the SBA 504 program is specifically designed for fixed-asset acquisition, such as purchasing the real estate where a franchise operates. This is a critical strategy for long-term wealth building, as it allows franchisees to act as their own landlords, building equity in the property while operating the business. According to industry data, franchisees who own their real estate have a significantly higher survival rate during economic downturns due to the stability of their occupancy costs.

Conventional Financing and the Threshold of Scale

As franchisees transition from "mom-and-pop" operations to multi-unit enterprises, their financing needs often outgrow the SBA’s limits. Conventional commercial lending becomes the next logical step. These loans are not backed by government guarantees and therefore require more stringent collateral and higher liquidity from the borrower.

Conventional lenders typically seek a Debt Service Coverage Ratio (DSCR) of 1.25x or higher, meaning the business’s net operating income must be at least 25% greater than its annual debt obligations. For established operators with five or more units, conventional financing can offer lower interest rates and fewer reporting requirements than SBA loans. However, the "barrier to entry" for conventional capital is high, often requiring a minimum of two to three years of profitable tax returns and a robust balance sheet.

Addressing the Capitalization Gap: Startup and Equipment Financing

One of the most frequent causes of franchise failure is undercapitalization during the "ramp-up" phase. New operators often focus exclusively on the initial franchise fee and construction costs, neglecting the "soft costs" that accrue before a location reaches its break-even point. These costs include local marketing, employee training, inventory stocking, and the "working capital cushion" needed to cover losses during the first six to twelve months of operation.

Equipment financing has emerged as a vital tool to bridge this gap. By utilizing lease-to-own structures or equipment loans, operators can preserve their cash for operational needs rather than tying it up in depreciating assets like ovens, fitness machines, or automotive lifts. Furthermore, Section 179 of the tax code often allows businesses to deduct the full purchase price of qualifying equipment in the year it is placed in service, providing an immediate tax benefit that can be reinvested into the business.

The Multi-Unit Expansion Chronology

The path to becoming a multi-unit mogul is rarely linear. It typically follows a structured chronology that lenders monitor closely:

- The Proof of Concept Phase: The operator successfully launches the first unit, demonstrating the ability to follow the franchisor’s system and manage labor and COGS (Cost of Goods Sold).

- The Infrastructure Phase: Before opening a second or third unit, the operator must invest in "above-store" leadership, such as a district manager or a centralized bookkeeper. Lenders look for this infrastructure as a sign that the operator is prepared for the complexity of multi-unit management.

- The Consolidation Phase: Once an operator reaches five to ten units, they often seek to refinance disparate high-interest loans into a single, cohesive credit facility. This simplifies the balance sheet and often lowers the weighted average cost of capital.

- The Institutional Phase: Large-scale operators (20+ units) may eventually attract private equity investment or move toward "recapitalization," where they take out equity to fund massive territorial acquisitions.

Market Analysis: Impact of Inflation and Interest Rates

The franchise financing landscape in 2024 and 2025 is being heavily influenced by the Federal Reserve’s monetary policy. With the "cost of money" significantly higher than it was in the previous decade, the margin for error in franchise operations has narrowed.

A one-percent increase in interest rates on a $2 million loan can result in an additional $20,000 in annual interest expense. For a business with a 10% profit margin, that operator must generate an additional $200,000 in top-line revenue just to maintain the same net income. This reality has forced lenders to be more selective, favoring "recession-resistant" sectors such as automotive repair, healthcare services, and quick-service restaurants (QSR) with strong drive-thru components.

Common Pitfalls and Strategic Recommendations

Christopher Cornella, Vice President of Business Development at US Medical Funding and US Professional Funding, emphasizes that many franchisees sabotage their growth by focusing on the wrong metrics. "The cheapest money is not always the best money," Cornella notes. "A slightly higher interest rate with a longer amortization period or no prepayment penalty can provide the flexibility needed to weather a temporary market dip or pounce on an acquisition opportunity."

Key mistakes identified by industry experts include:

- Waiting Too Late: Many operators wait until they are in a cash crunch to apply for a line of credit. Banks are most willing to lend when the business doesn’t desperately need the money.

- Poor Financial Hygiene: Inconsistent bookkeeping or "co-mingling" personal and business expenses can lead to immediate rejection during the due diligence phase of a loan application.

- Ignoring the "Exit Strategy": Lenders want to see a clear path to repayment. Operators who have a 10-year plan that includes eventual sale or succession are viewed as more stable risks.

The Broader Economic Implications

The health of the franchise financing market serves as a bellwether for the broader economy. When capital flows freely into franchising, it signals confidence in consumer spending and local employment. Conversely, a contraction in franchise lending often precedes a broader economic cooling.

As the industry moves forward, the integration of Artificial Intelligence in underwriting and the rise of "FinTech" lenders are expected to speed up the approval process. However, the fundamental principles of lending remain unchanged. Lenders are looking for "professional operators" rather than "passive investors." They seek businesses that demonstrate a mastery of unit economics and a clear strategy for sustainable growth.

In conclusion, while the franchise model provides the engine for business ownership, strategic financing provides the fuel. For the ambitious franchisee, capital is not merely an expense; it is a strategic tool that, when used correctly, allows for the transformation of a single storefront into a diversified and resilient portfolio of assets. Understanding the lender’s perspective is no longer an optional skill—it is a prerequisite for survival in the competitive modern marketplace.